Cover image created through Copilot

As is known to all, diversification is the key to managing the risk of your investment. However, it’ll take a lot of effort and time to hand-pick quality assets that have little correlation with each other. In the Hybrid Asset Allocation trading strategy, Wouter J. Keller and Jan Willem Keuning actually brought up an easier way to introduce diversification into the trading strategy. In this article, we’re going to first talk about HAA strategy and see how it boosts the diversification of our portfolio. Then, we’re also going to backtest the HAA (Hybrid Asset Allocation) trading strategy and several of its variations against the benchmark.

Become a Medium member to support me in writing more interesting articles. I’ll receive a small portion of your membership fee if you use the following link, at no extra cost to you.

If you enjoy reading this and my other articles, feel free to join Medium membership program to read more about Quantitative Trading Strategy.

Previous researches

- From Theory to Profits - Elevating the Buy-on-Gap Strategy with Advanced Techniques

- Optimize your MACD strategies with advanced indicators

- 【Pair Trading】 Complete Guide to Backtest Cointegration Pair Trading Strategy

- 【ML algo trading】 II - How to build a machine learning boilerplate?

What is Hybrid Asset Allocation (HAA)

Hybrid Asset Allocation (HHA) was first introduced in Dual and Canary Momentum with Rising Yields/Inflation: Hybrid Asset Allocation (HAA) from SSRN in Feb 2023. The intention is to develop a much simpler strategy for the retail investors. This strategy is balanced and rather aggressive compared to the author’s previous trading strategy. It uses US Treasury Inflation-Protected Securities (TIPS, ETF: TIP) as the canary asset to determine whether the market possesses positive momentum. Once the canary asset shows positive momentum, we shall invest the offensive assets to profit. Otherwise, we invest the defensive asset to further protect against loss.

This strategy not only uses the single canary asset as the market momentum indicator. In the meantime, it also adopts the traditional dual momentum method to further confirm which assets we should invest among our offensive assets. Combining these two methods, its simplicity greatly reduced the possibility of unintentional overfitting, leaving much room for the intelligent retail investor to compose and customize their asset universe that could be potentially more aggressive or risk-averse.

How HAA adds diversification to our portfolio

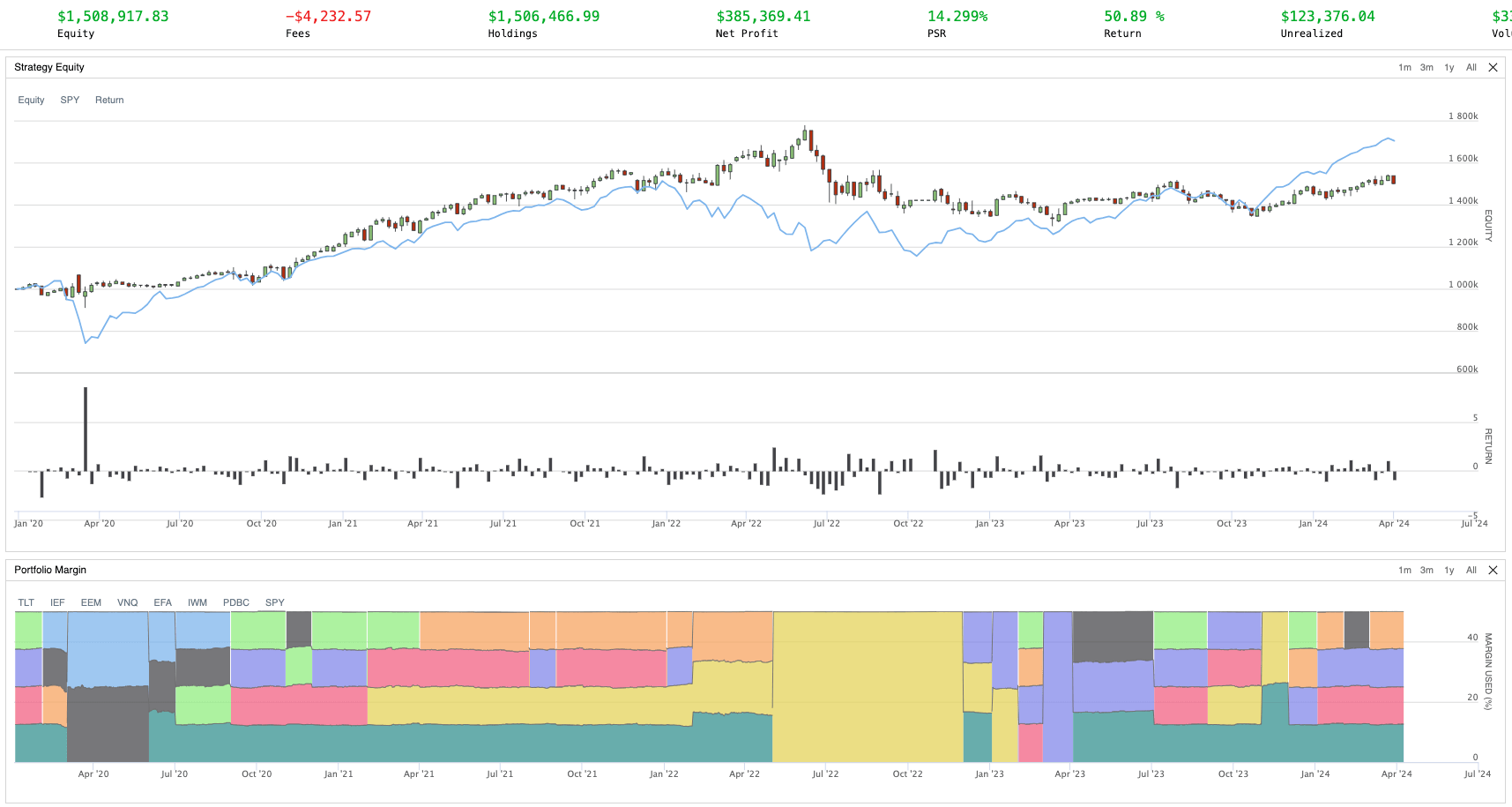

Even though the canary asset is the crucial part of the strategy that helps identify the current momentum trend of the market, the actual power of risk-aversion resides inside the assets picked: the ETFs in the offensive assets. These eight assets US large caps (represented by SPY), US small caps (IWM), developed international stocks (EFA), emerging market stocks (EEM), US real estate (VNQ), commodities (PDBC), intermediate-term US Treasuries (IEF) and long-term US Treasuries (TLT) in the offensive assets represent the strong and quality stocks worldwide covering most of the industries. This diverse universe is the part that adds diversity to our portfolio.

Backtesting HAA and its variations

Now let us have a look at our backtesting setup.

Platform

I’m using QuantConnect to backtest this strategy.

Backtest period

I’m conducting two series of backtests. One from 2016-01-03 to inspect the strategy performance as much as possible. The other one is from 2020-01-03 to inspect the recent changes and to compare it with the previous series.

Trading Framework

Universe

- Canary asset: US Treasury Inflation-Protected Securities (TIPS, ETF: TIP)

- Offensive assets: US large caps (represented by SPY), US small caps (IWM), developed international stocks (EFA), emerging market stocks (EEM), US real estate (VNQ), commodities (PDBC), intermediate-term US Treasuries (IEF) and long-term US Treasuries (TLT)

- Defensive asset: intermediate-term US Treasuries (IEF)

Strategy Benchmark

In the article Hybrid Asset Allocation, the 60/40 benchmark was constructed by 60% of SPY and 40% of IEF. To look at the strategy from a more aggressive angle, I use simply the SPY buy-and-hold strategy as the benchmark, which also helps identify the stock market situation.

Trading Rules

- The definition of momentum is defined as the unweighted average return of one-month, three-month, six-month, and twelve-month returns (in %)

- All the positions are created and closed right after the market opens.

- If the canary asset shows positive momentum, we pick the four ETFs with the highest momentum from offensive assets to invest evenly.

- Otherwise, we allocate our capital to defensive asset.

- We rebalance our portfolio every month.

Formula to calculate the momentum

Variation Strategies

There are two switches that I added to this HAA strategy. First is whether to disable the canary asset indicator that we used to detect the market momentum. Once we switch this off, we simply purchase four ETFs that have the highest momentum from the offensive assets no matter the market momentum, turning this strategy into a pure ETF momentum strategy. Second, I added an additional filter to rule out those ETFs whose momentum ranks top four but is actually negative. Below is the backtest results.

Results

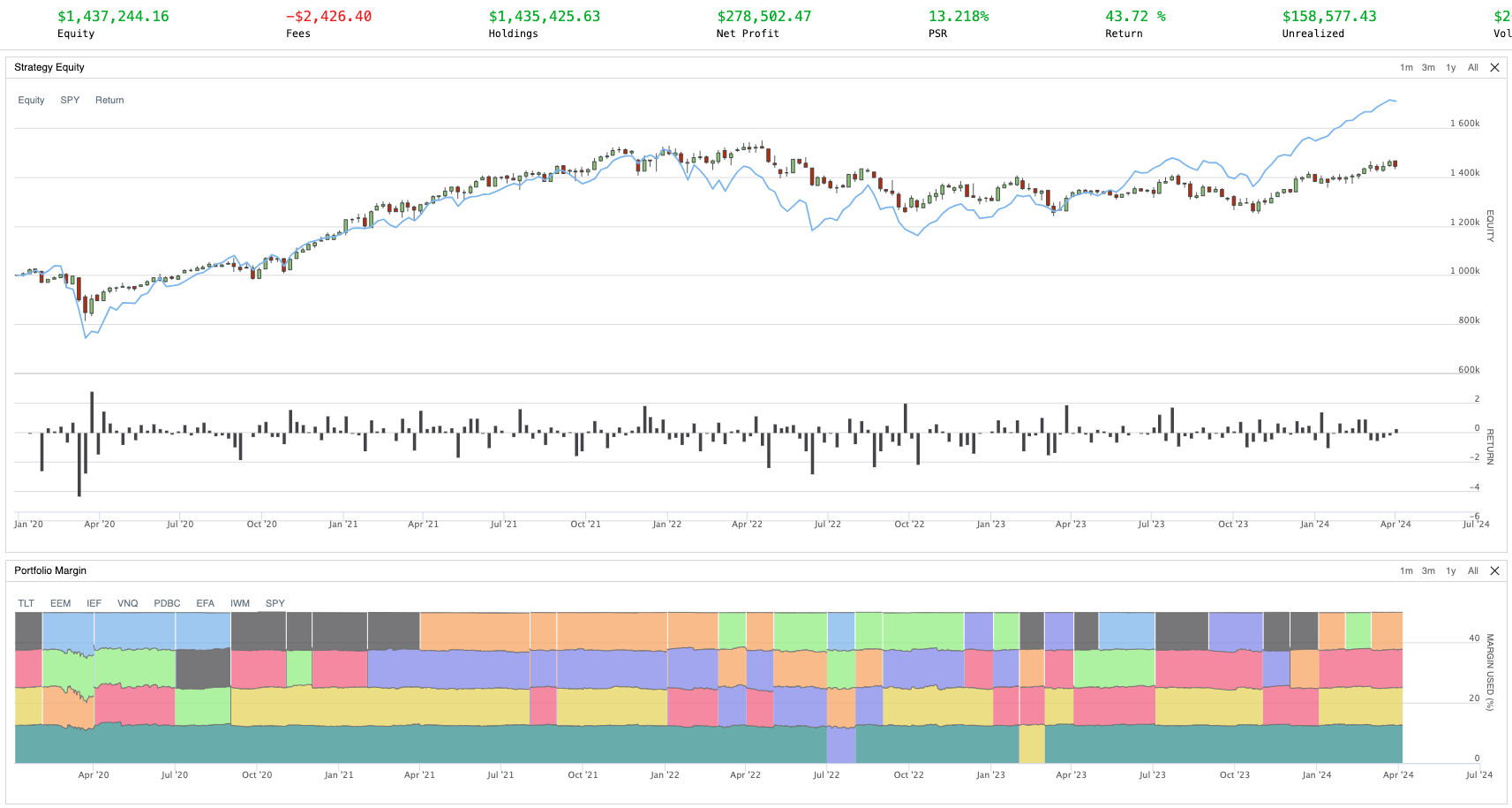

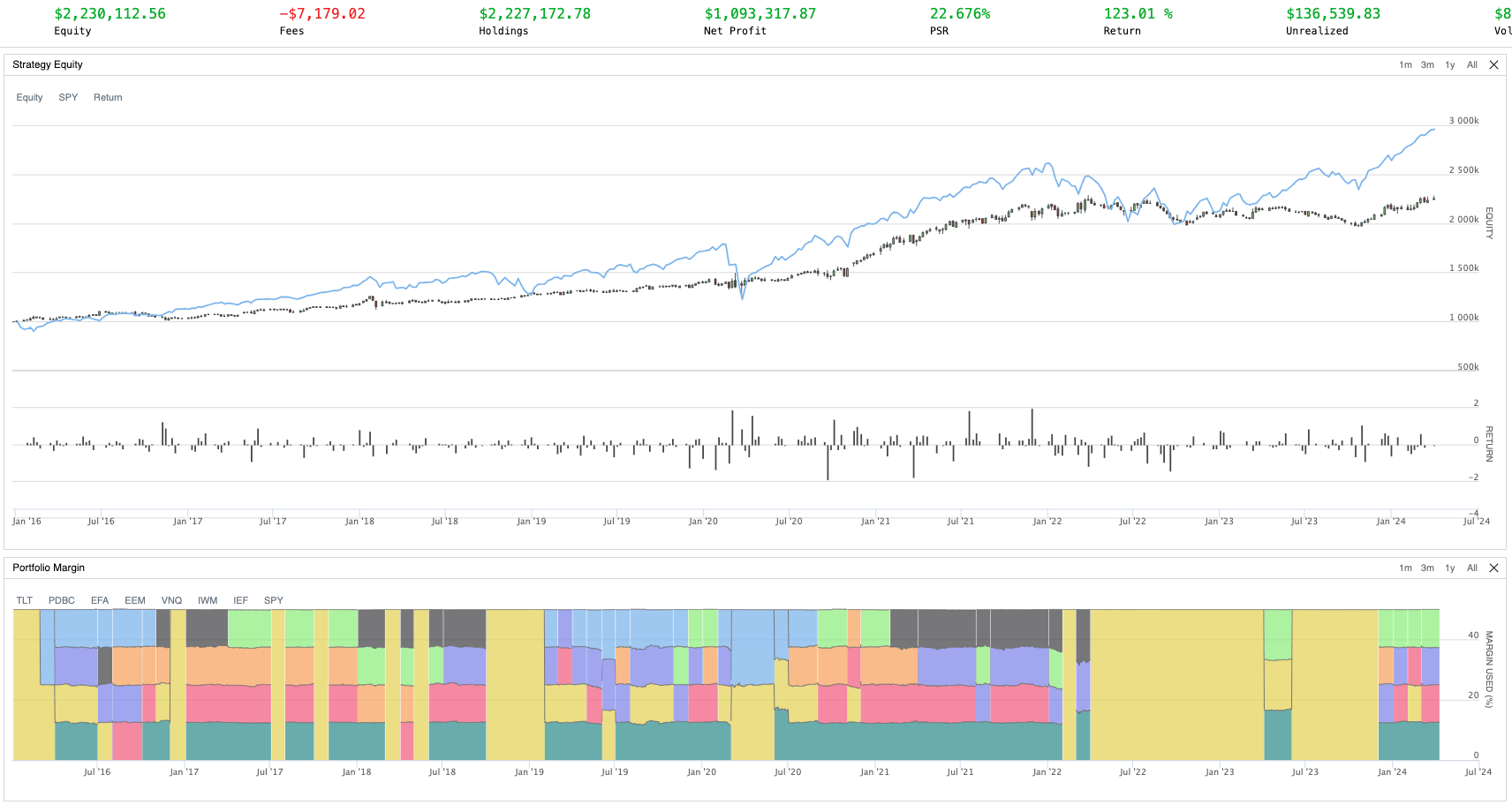

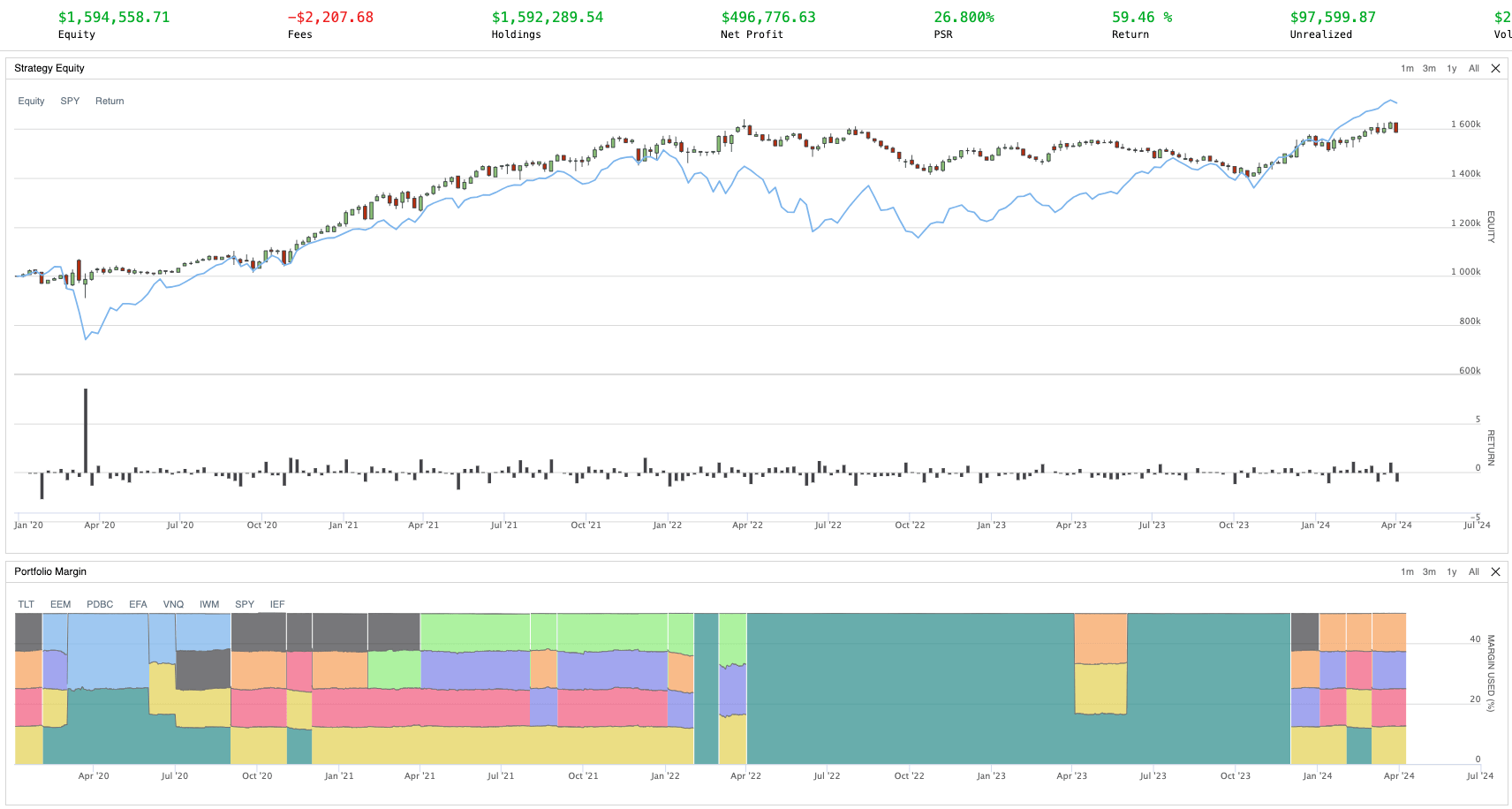

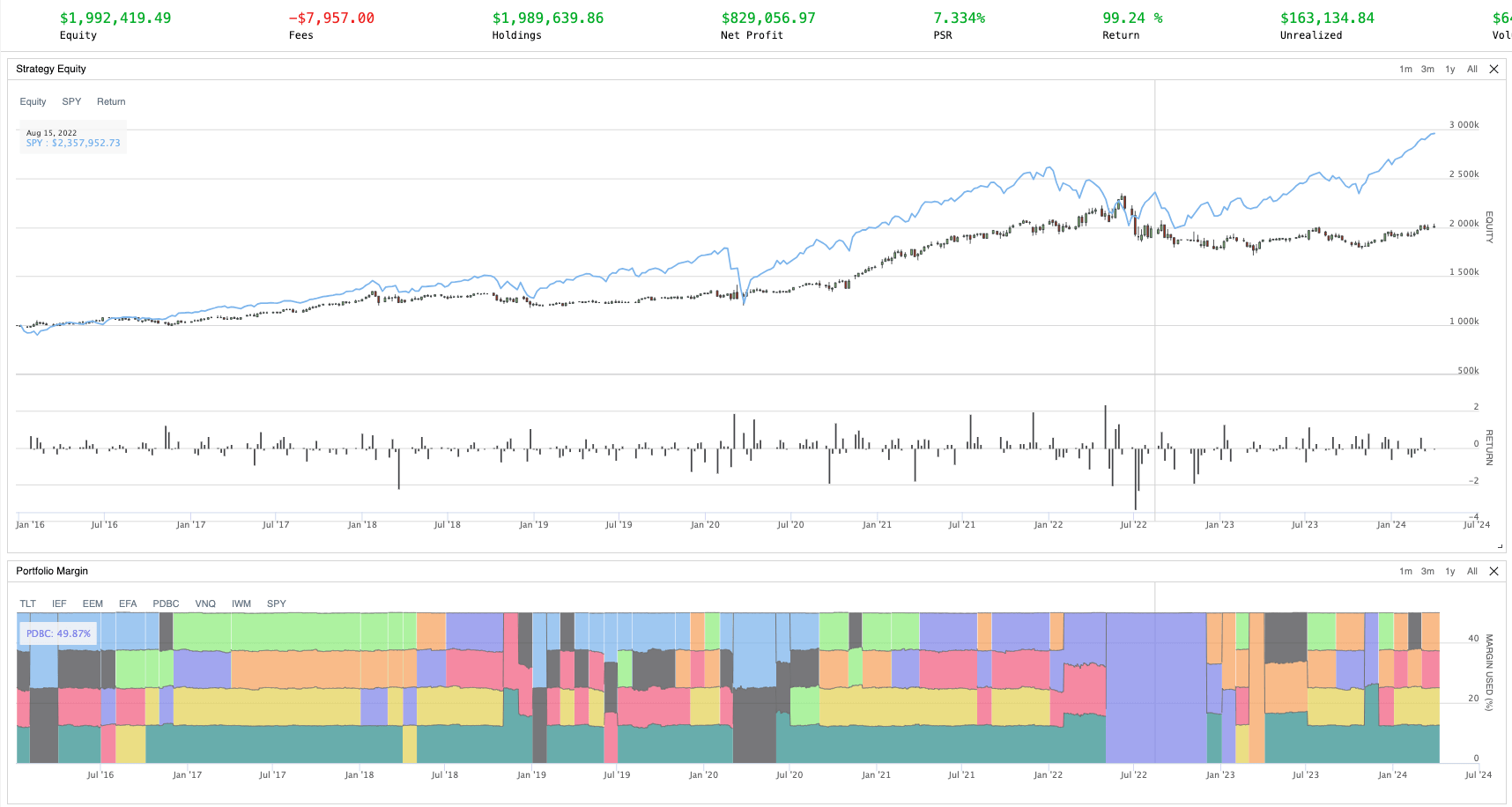

| Year start | 2016~ | 2020~ |

|---|---|---|

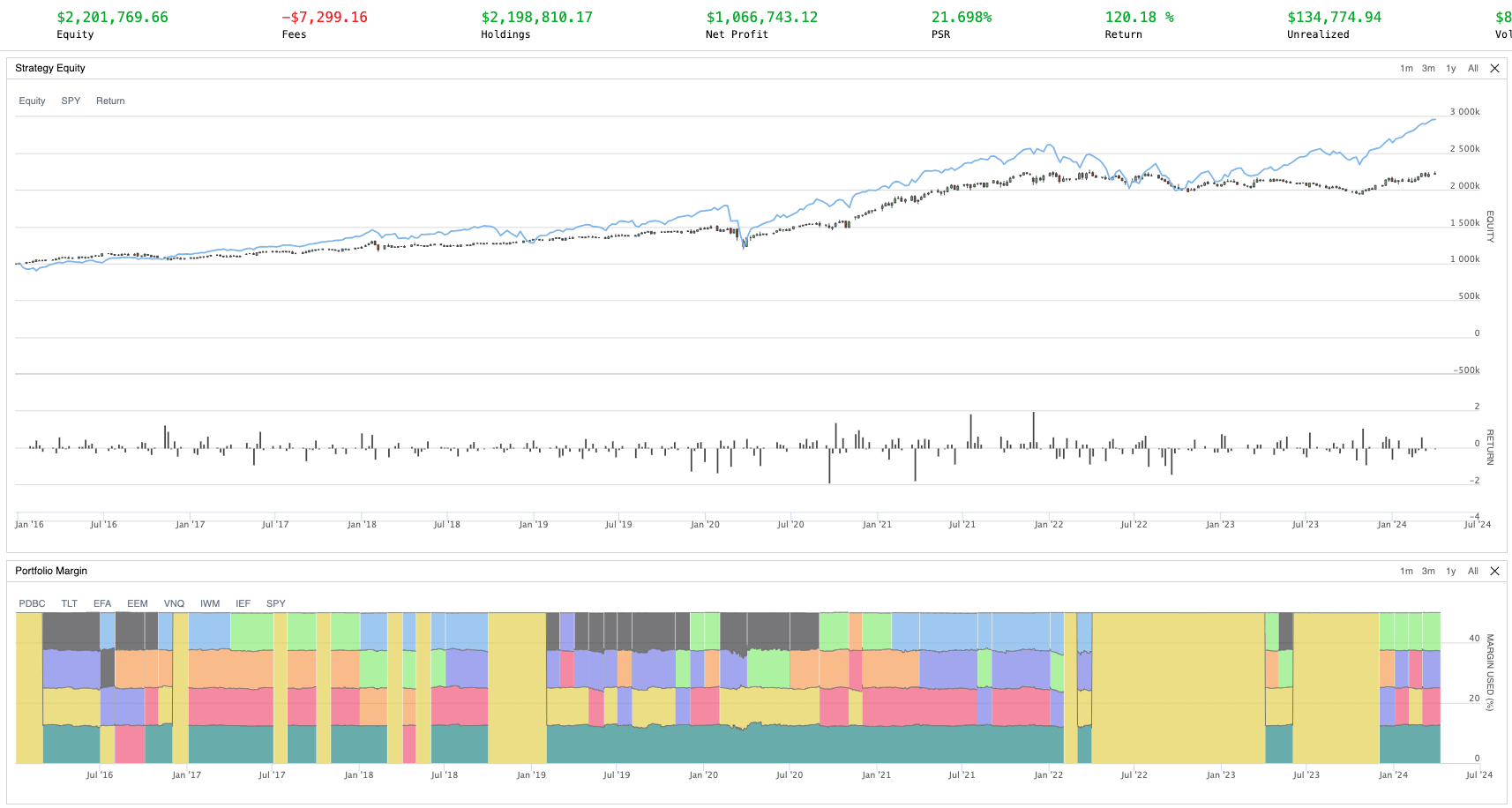

| HAA basic |  |

|

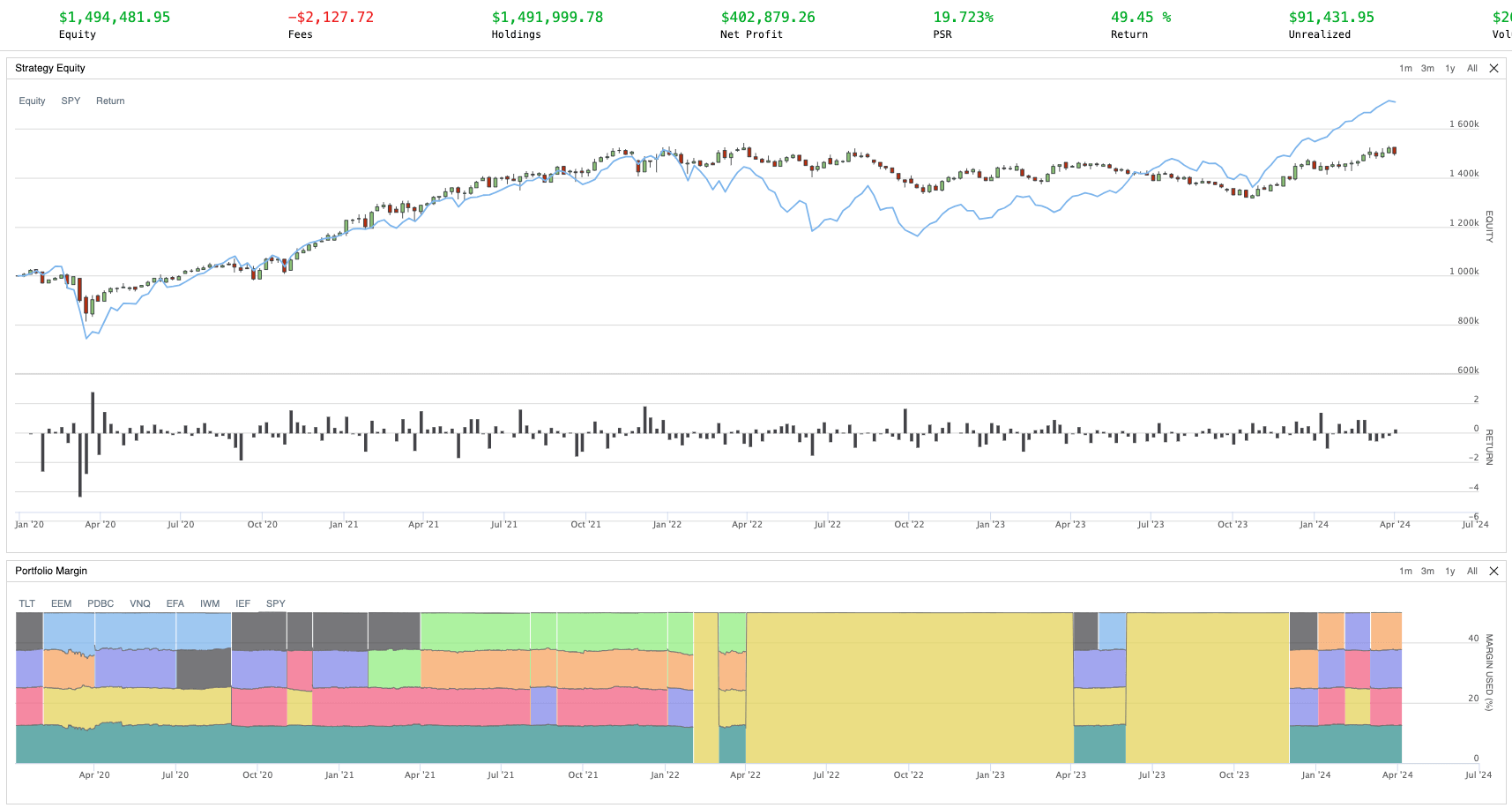

| HAA ignore canary |  |

|

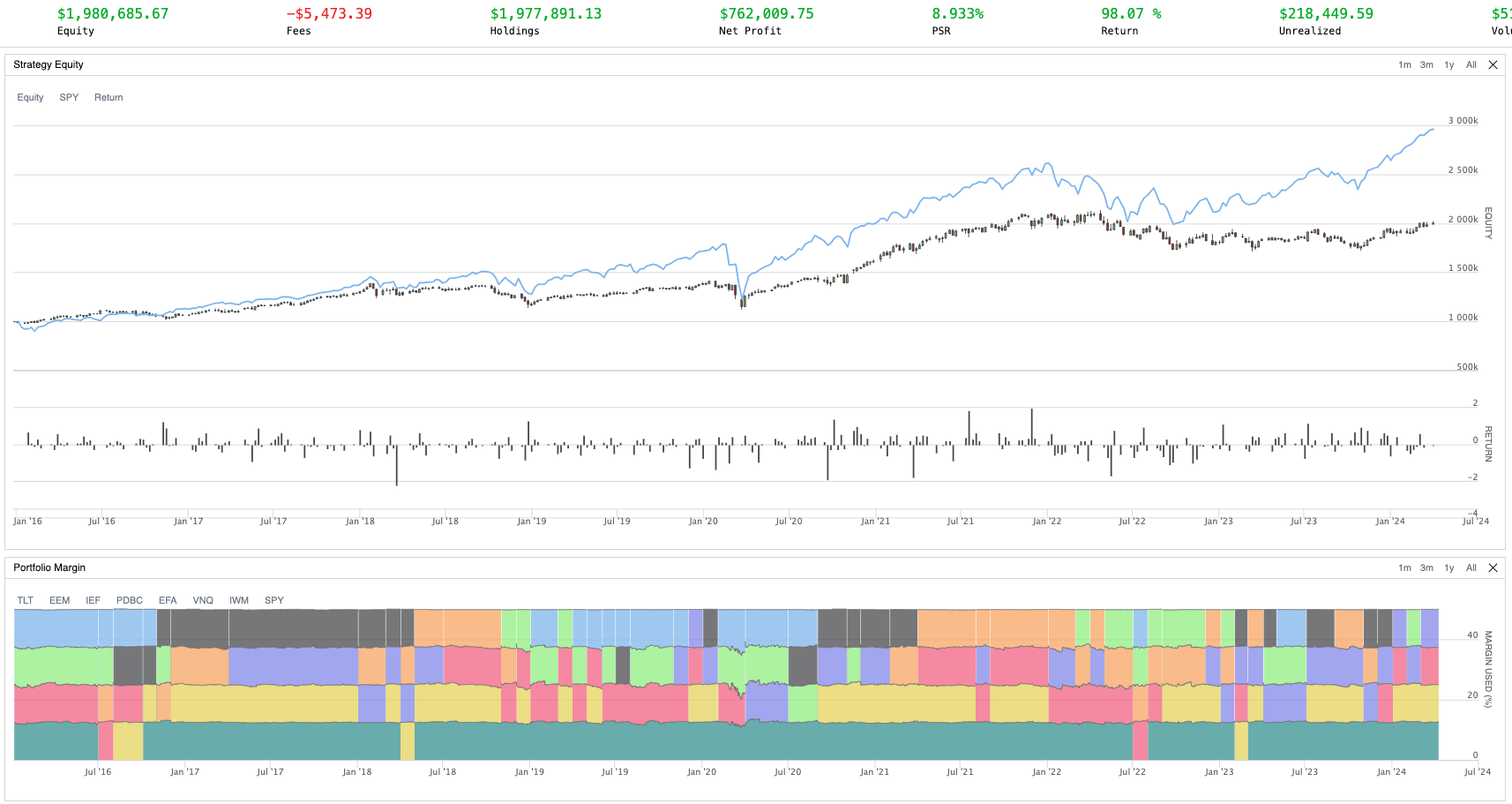

| HAA ignore negative |  |

|

| HHA ignore both |  |

|

Backtesting HHA and its variations against SPY buy-and-hold strategy

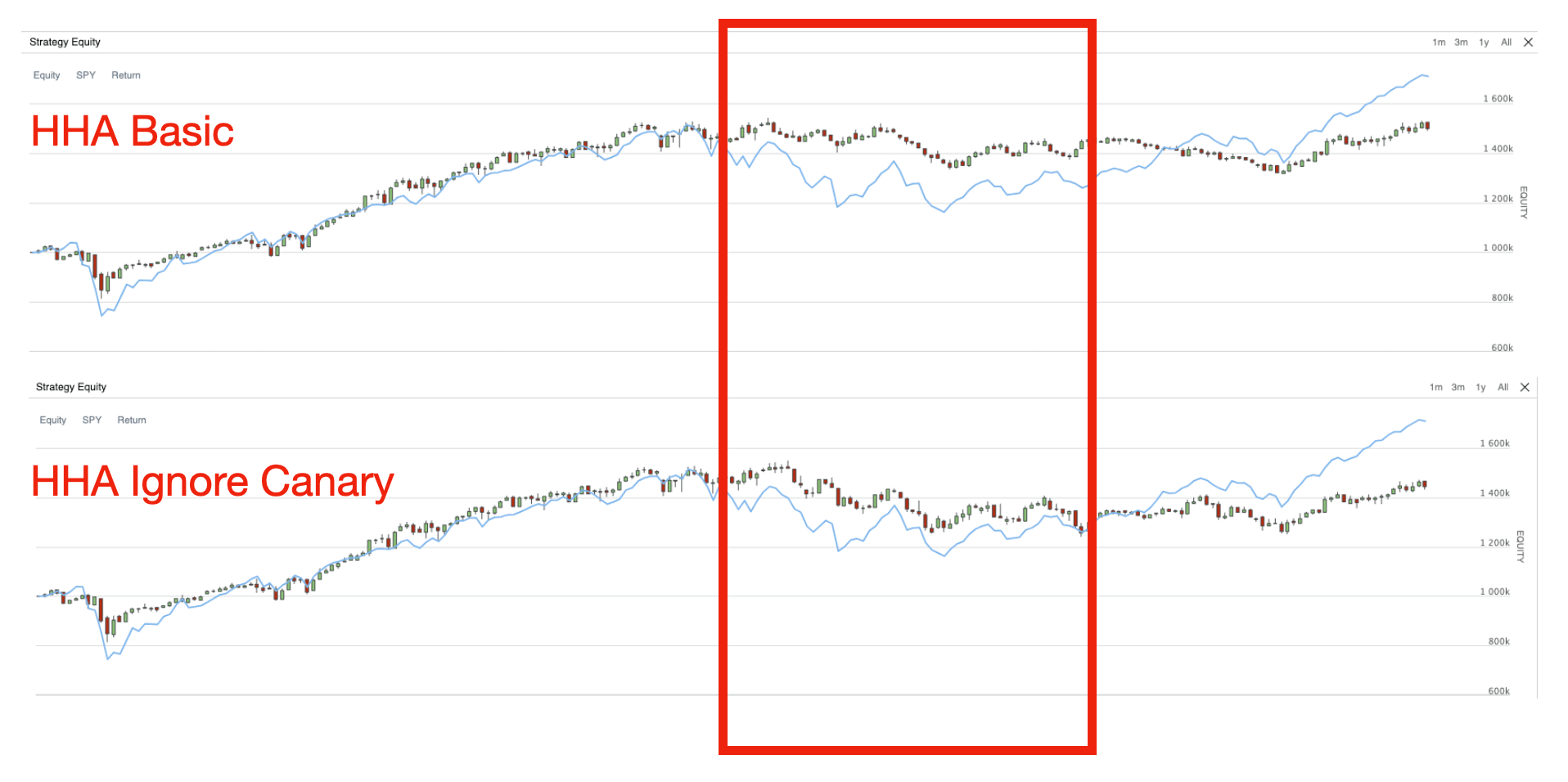

If you look at the backtest results carefully, you’ll notice that none of the HAA strategy and its variations exceeds the performance of the benchmark SPY buy-and-hold strategy. However, the HAA strategy would help us avoid the loss during the market setback and grow the investment steadily. Take the basic HAA strategy backtest results since 2020 for example. Compared to the HAA ignore canary scenario, our canary asset seems to be able to identify the market turmoil so that our investment focus will turn to the defensive asset to avoid further loss.

Basic HAA V.S. HAA ignore canary asset since 2020

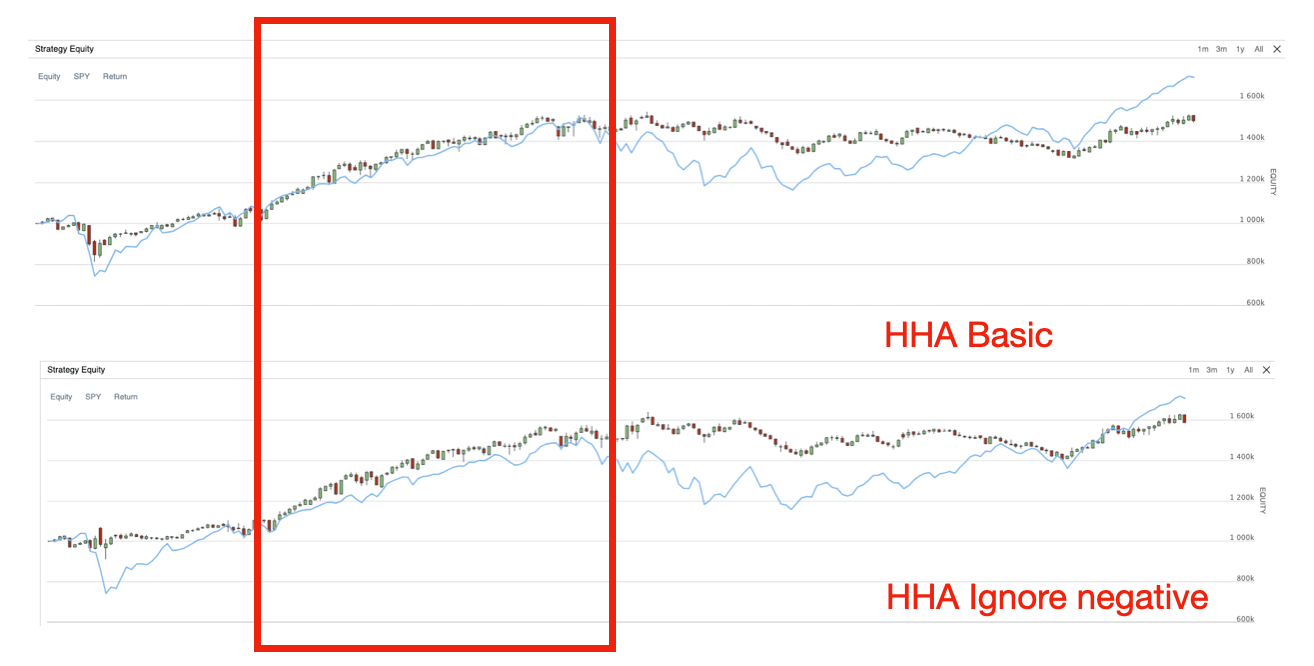

Besides, if you compare the basic HAA strategy with the HAA ignore negative strategy, you will see that the HAA ignore negative strategy indeed slightly outperforms the HAA basic strategy for a certain period.

Basic HAA V.S. HAA ignore negative strategy since 2020

| 2020 | Benchmark (SPY buy-and_hold) | HAA basic | HAA ignore canary | HAA ignore negative | HAA ignore both |

|---|---|---|---|---|---|

| Annualized Return | 13.553% | 9.892% | 8.889% | 11.554% | 10.120% |

| Annualized Volatility | 0.138 | 0.109 | 0.121 | 0.108 | 0.133 |

| Sharpe Ratio | 0.48 | 0.473 | 0.382 | 0.578 | 0.422 |

| Sortino Ratio | 0.491 | 0.523 | 0.423 | 0.699 | 0.451 |

| Max DD | 33.600% | 18.900% | 19.400% | 14.000% | 26.200% |

| Number of orders | 1 | 143 | 210 | 131 | 163 |

Stats HHA and its variations against SPY buy-and-hold strategy (since 2020)

| 2016 | Benchmark (SPY buy-and_hold) | HAA basic | HAA ignore canary | HAA ignore negative | HAA ignore both |

|---|---|---|---|---|---|

| Annualized Return | 14.128% | 10.014% | 8.615% | 10.184% | 8.693% |

| Annualized Volatility | 0.151 | 0.091 | 0.103 | 0.091 | 0.111 |

| Sharpe Ratio | 0.579 | 0.568 | 0.423 | 0.581 | 0.406 |

| Sortino Ratio | 0.573 | 0.597 | 0.447 | 0.653 | 0.423 |

| Max DD | 33.7% | 18.900% | 19.400% | 14.000% | 26.200% |

| Number of orders | 1 | 310 | 374 | 295 | 324 |

Stats HHA and its variations against SPY buy-and-hold strategy (since 2016)

Based on the provided stats above, the HAA strategy and its variations did mitigate the annualized volatility and decrease the maximum drawdown drastically. Yet, the annualized return also shrank along with the decrease of the volatility. Combining both the chart and tables above, the Sharpe ratio and Sortino ratio both improved after we adopted the HAA ignore negative scenario by removing the ETFs that have negative momentum from our target ETFs. This would be an interesting case to further explore.

Conclusion

HAA seems to be a strategy that tries to exploit the advantage of diversification. In the meantime, adding the ETF element to the universe would further elevate the quality level of the universe as the stocks constituted by the ETF are deliberately chosen. As the next step, maybe we can try to find a better diversified ETF to represent the other industries and other aspects of the entire market, improving further the portfolio performance in the future.