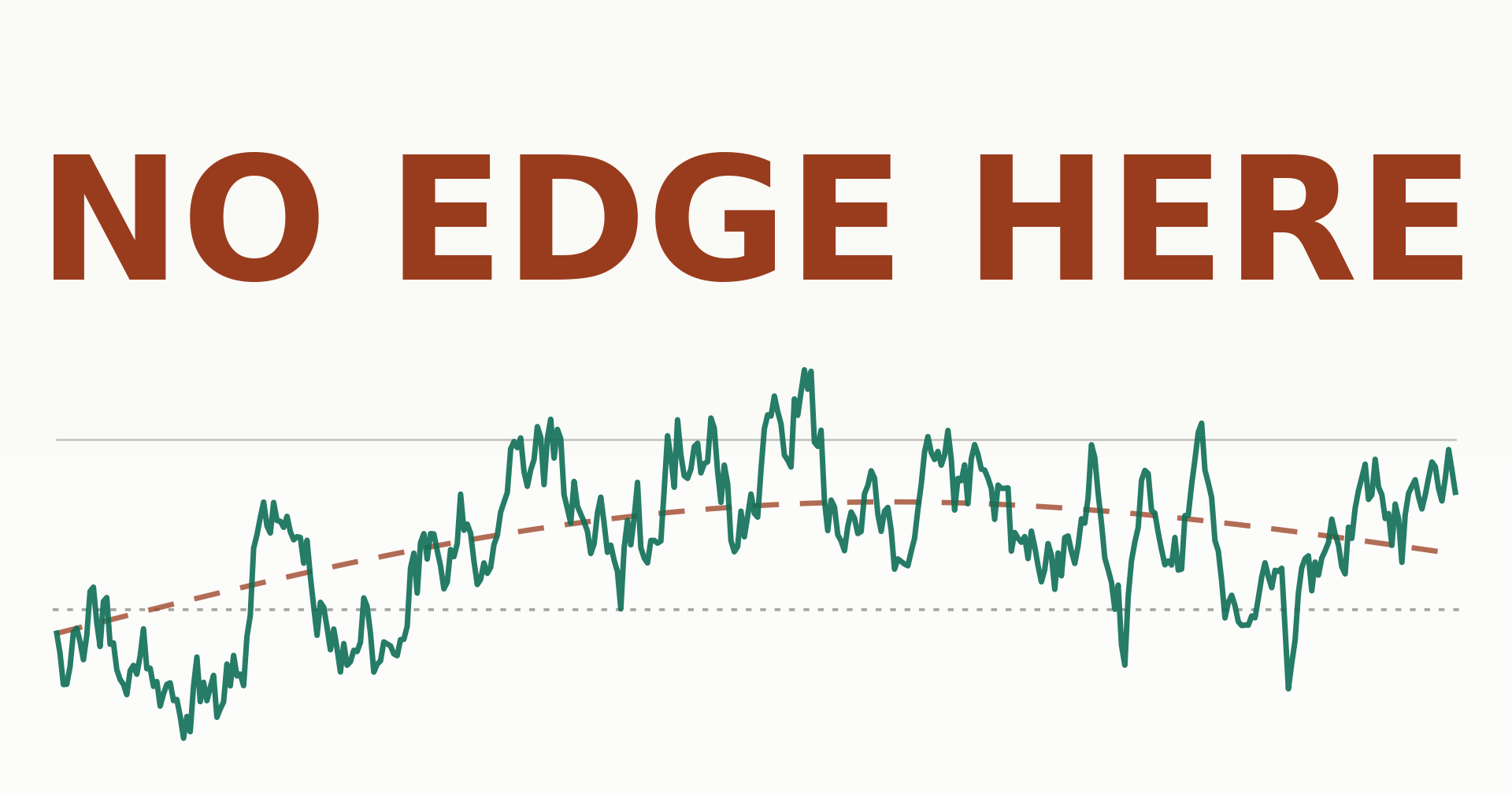

Ever built something so carefully that its most valuable answer turned out to be “no”?

That’s pretty much the story of my last few weeks. I went looking for edge in the mean reversion behind pairs trading — the whole statistical-arbitrage playbook — and built a framework as rigorous as I could to test the idea honestly instead of flatteringly. Then I ran it on three different asset universes, one after another, and the backtest results failed me three times in a row.

This whole project started life as my final project for the CQF (Certificate in Quantitative Finance). I passed — but when I handed it in, I had that nagging feeling that I’d rushed it, and that I could do it far more thoroughly if I actually gave it the time it deserved. A couple of months later, I went back, rebuilt the framework from scratch, and let it run on real data until it told me something I didn’t want to hear. This post is the story of those three rejections — stocks, ETFs, and commodity futures — and why I’ve come around to thinking of this carefully built framework like the manager who rejects every proposal you bring him… and turns out to be right every time.