Value investing is an investing strategy that has been popular for decades. The main idea involves picking quality stocks among distressed companies, buying and holding them for the long-term (over several years), and expecting the good quality stocks to remain good and rebound from the valley. In short, value investing is to buy good companies at a good price. In this post, we’re going to go through the framework that some of the value investors use to evaluate the company value.

What exactly is Value Investing?

Warren Buffett is probably the most well-known value investor today, but there are also many other value investors in the field, such as Benjamin Graham (Buffett’s mentor), Charlie Munger (Buffett’s business partner), and Joel Greenblatt. Among them, Benjamin Graham is highly praised as the “Father of Value Investing“ and has a significant place in the field. There are also famous case studies such as Buffett’s bet on Coca-Cola in 1988 and Geico in 1951, which both generate a massive return. In addition, the previous post of An investment strategy that takes you three days a year was also derived from the magic formula that was created by Joel Greenblatt.

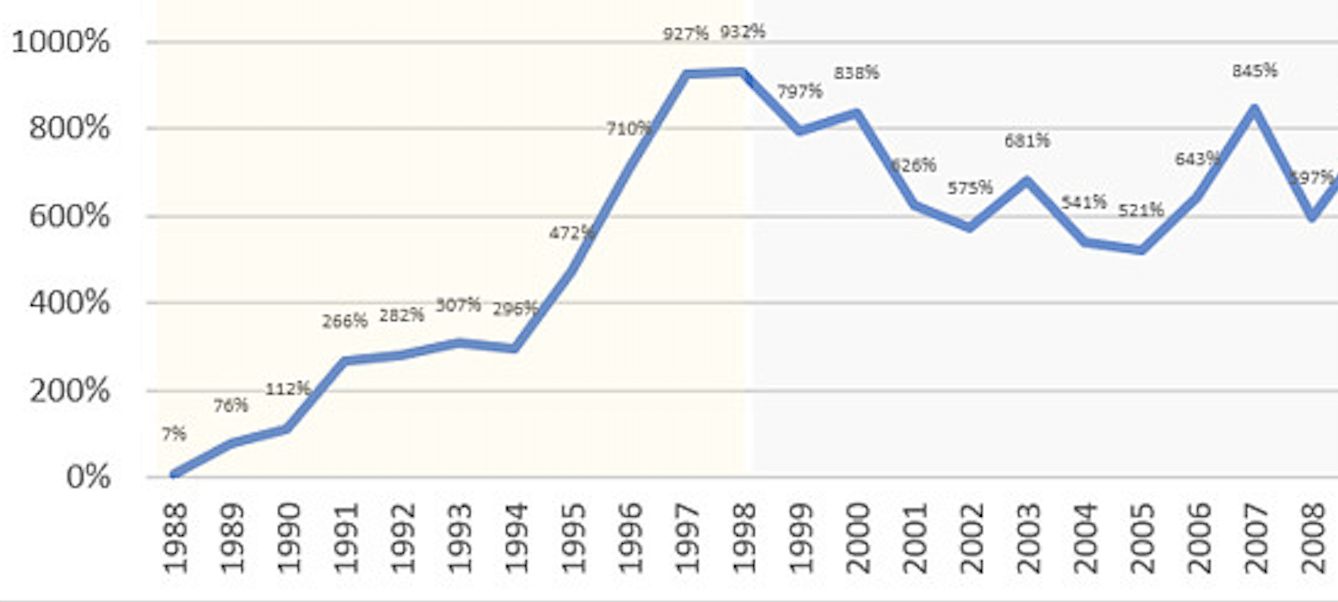

The stock price of Coca-Cola since 1988

Value investors advocate the idea of finding the stocks whose market value (stock price) are traded way lower than their company intrinsic value. By using the data from fundamental analysis and company annual reports every year, value investors would use their framework to calculate the company intrinsic value with assuming growth rate for the upcoming years. If the gap (which was so called “safety margin“) between the market value and the calculated intrinsic value is larger enough, it is believed that the discounted market value is simply due to public opinions and emotions. The company itself is still healthy enough to generate positive net income to grow continuously, pumping its stock price back to where it should be or even higher.

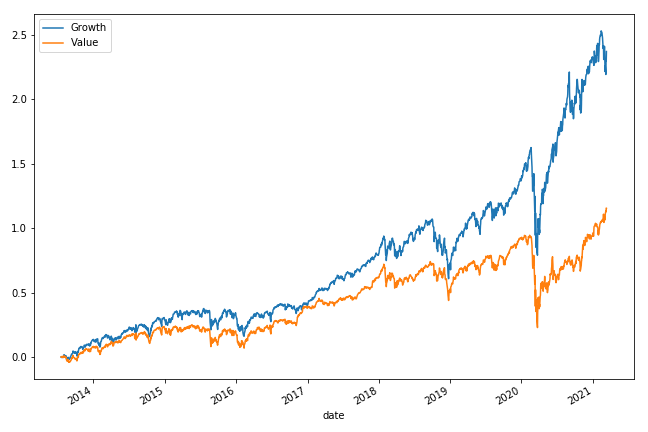

In recent years, analysts and investors are saying that the value stocks are no longer attractive and throwing themselves into growth stocks’ arms such as FAANG, Tesla, Roku, and so on. However, there are still others who believe that the value investing was still profitable because:

- The economic cycle is extended. So the stocks you invested simply need more time to rebound. See here

- The profit was diluted because the value investing strategy is too well-known and was adopted by too many investors and investing institutions. See here

Value stocks v.s. growth stocks in recent years

Either way, I believe that there are some ideas inheres within the value investing strategy itself which are still valuable and beneficial in adopting them into the quantitative strategies. So now, let’s have a look.

The evaluation framework of Value Investing

There are a lot of methodologies and frameworks that were developed within Value Investing. The book “Value Investing: From Graham to Buffett and Beyond“ by Bruce C.N. Greenwald, Judd Kahn, Paul D. Sonkin, and Michael van Biema promotes a framework that separates the whole evaluation process into several stages: 1. calculate the Asset Value (AV) of the company, 2. calculate the Earnings Power Value (EPV) of the company, 3. compare to the market value and see whether we’ll be able to make the decision to invest in this company or not.

Asset Value (AV)

The Asset Value is calculated to evaluate the actual value of the company, including tangible assets and intangible assets. Tangible assets include PPE, marketable securities, inventory, and so on. They can be found in the balance sheet in the annual/quarter report. However, the one-the-book asset value doesn’t reflect its value right now, so we need to make adjustments on these items in order to find out the current value of the company asset.

Intangible assets include goodwill, brand value, workforce, product portfolio, clients/contracts, and everything. As most of these assets are not documented in the balance sheet, we need to figure out a way to estimate the ballpark amount of these items. For example, the workforce cost is already included in the SG&A in the balance sheet but not the HR cost on recruiting this workforce. Therefore, if there is a company A that has 1,000 blue-collar workers, we can take the US average wages of blue-collar workers to calculate the total cost.

According to www.comparably.com

We assume the cost to recruit the workforce is 10% of the total cost of the workforce, then we’ll be able to calculate the cost of the recruitment to be:

This would be one of the adjustments that we made while calculating the company asset value.

Earnings Power Value (EPV)

Earnings Power Value essentially means the capability of a company to make money, and it’s not just any money that a company makes. We’re looking for Net Operating Profit After Tax (NOPAT), meaning the income from financial activities and from investing activities. The NOPAT of a company could showcase the ability to earn net income through selling the company’s services or products. After all, selling services and goods to the customers is the major business activity of the company.

Also, we need to make sure the company can sustainably make this amount of money or more. If a company’s NOPAT fluctuates a lot, this would implicitly indicate that the company business is not stable enough to support sustainable growth.

A quick way to explain the way to calculate the EPV is:

Lastly, since we have been able to approximately evaluate the NOPAT of the company we can use DCF (Discounted Cash Flow) model to calculate the EPV of the company. We use the Weighted Average Cost of Capital (WACC) as the discount rate in our calculation so that we take the actual cost of working capital into account. Then, we will get a number that represents the value of an investment that can generate this NOPAT steadily.

The final call on the decision

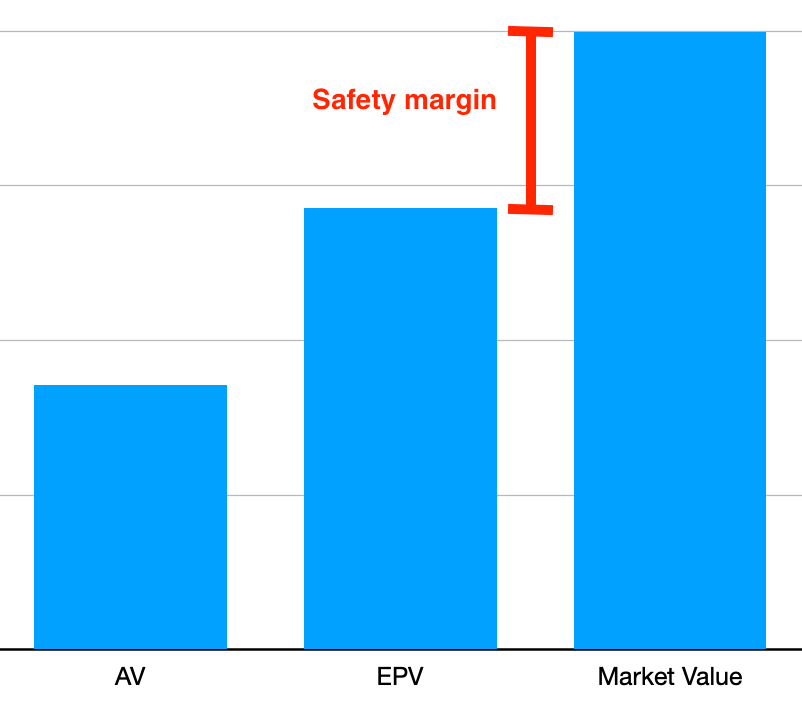

Once we have our AV and EPV ready, we can start making our final call on whether we should long this investment or not. Here’s a general principle to follow:

- If AV is higher than EPV, meaning the industry is declining and this company won’t be able to make enough profit as it’s mismanagement of its assets.

- If AV is equal to EPV, meaning this company is able to efficiently manage its asset to generate enough profit.

- If AV is below the EPV, meaning this company’s management team has a superior ability to manage its asset. Also, this indicates that this company has sufficient power to build the barriers to entry to outcompete the other competitors in this industry.

Then, we compare the EPV with the market value of the company to see whether this company is currently undervalued or overvalued. If it is undervalued, maybe this is the timing for us to enter this trade.

AV, EPV, and market value

Wrap up

What I have demonstrated above is only a part of the value investing methodology. There are more technics, assumptions, and methodologies involved that are too complex to be tuck into one single post. So I’ll stop it right here so that you can discover more by yourself.

A lot of people say that Value Investing is dying. But I think value investing is a tool and mindset, and also an essence of analysts’ experience. There are a lot of valuable thoughts that can be extracted and be applied to quantitative trading. For example, stock-picking to form your stock pool, evaluating a company to see it is under- or overvalued, and also processing the fundamental data to make it more meaningful to conduct a second analysis. I believe learning how value investors think would definitely benefit your capability to build an even better quantitative trading strategy.