In recent days, the financial markets across countries are tumbling. I got complaints from people saying that they lost money on some trades that look promising in the beginning. Also, some friends claimed that they made a small fortune with their unique insight in the turbulent days. Annoyingly enough, that people who made money from these trades tended to brag about how unique vision they possessed, and you can’t ignore the return they have achieved and crave the know-how how they pulled it off.

If you had enough of these, reading this research paper would make you feel better mentally, (sorry but won’t help you make more money right away) because these guys are just lucky enough to be born in the right era.

Introduction

The Artemis Capital Management L.P. published this research paper in January 2020, right before the COVID-10 virus burst out. This paper points out a few misunderstandings that consist of modern investment strategies and performance evaluation:

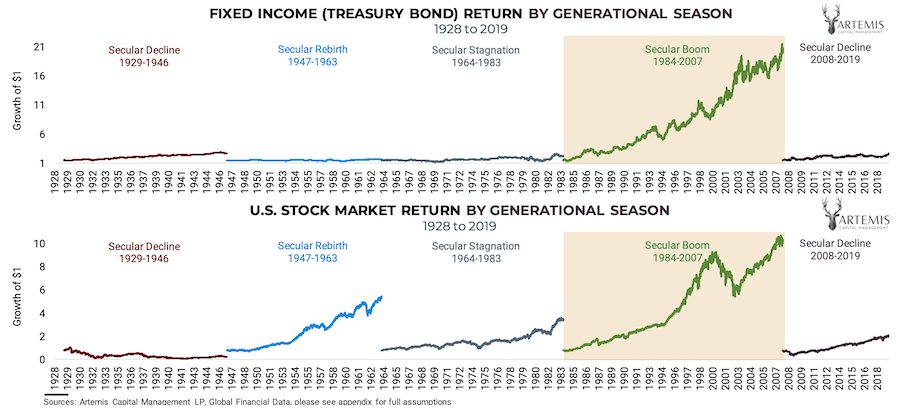

- Economic cycle/business cycle is longer than we think it is

The macroeconomic suggested that the economic cycle is either six years (internal economic cycle) or 10 years (external economic cycle), indicating that its stock price will rise every 6-10 years if this company stays long enough. Many investment strategies such as mean reversion strategy are developed based on this theory. However, the average age of an investment advisor is 52 years old, meaning the modern investment strategies have had been developed, polished, and validated less than four decades. This paper has separated the past ~90 years into four stages, and it’s quite clear that the market performed differently in either stage. This potentially tells us that we’re only looking at a limited time period while we evaluating our portfolio performance.

This is not REPEATABLE in the long run

As the trading data has been digitized in recent 2-3 decades, for many large quantitative asset managers do not test their strategies in periods without optimal data. Hence their recommended portfolio hasn’t been well validated with historical data, which is risky to the investors.The strategies look profitable simply because we’re living in the right time

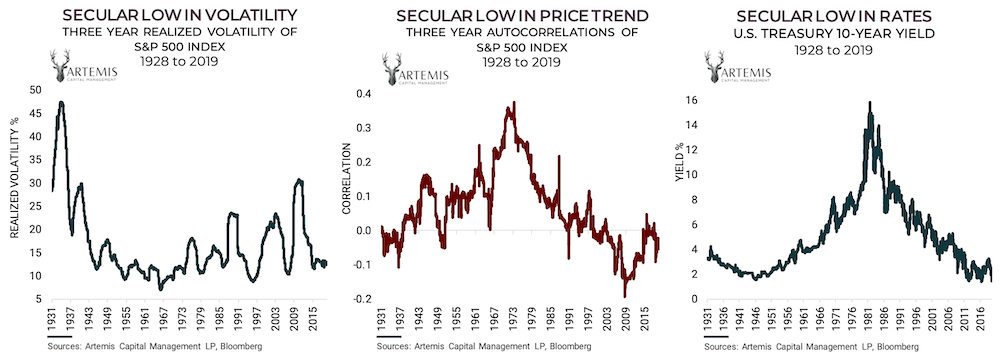

![]()

From the diagrams above, you can tell that we’re at an all-time low in 1. Volatility, 2. Asset Price Trending, and 3. Interest Rates for the recent decade. Therefore, many modern investment strategies generate yield based on the assumption that these core economic indexes won’t move away significantly. So applying the same strategies over 90 years would be extremely risky as the model has not been tested nor been hedged against the economic shifting.

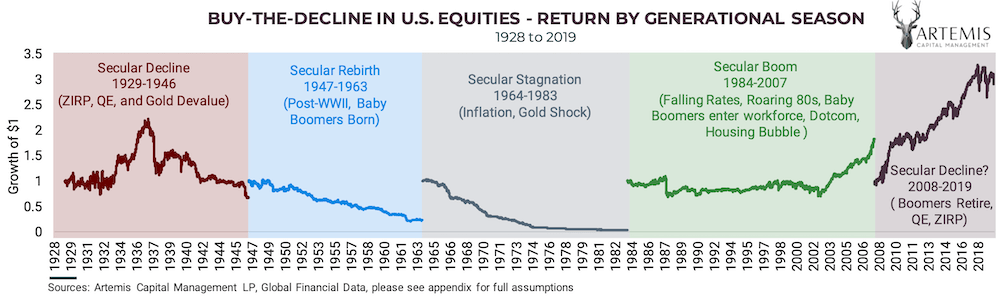

To put this in a more simple way to illustrate the seriousness of the consequence, if we adopted Buy-The-Dips strategy since 1928 to 1970, you would have been bankrupted THREE TIMES.In short, Buy-The-Dip is a popular strategy that buys any target stocks after the day that the Stock Market has fallen, expecting a rebound of the market and profiting from the recovery.

Allegory

In this research paper, it uses a very interesting metaphor to describe the market:

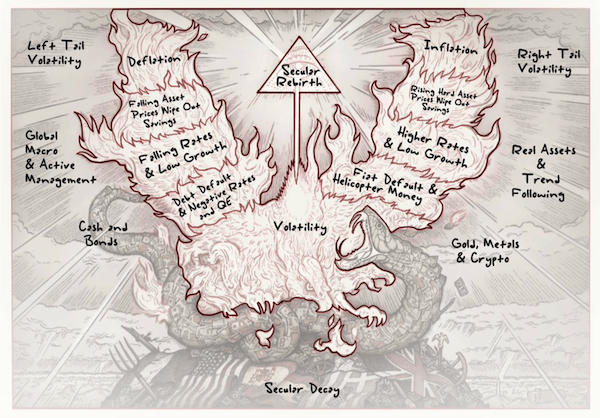

- Serpent represents secular growth. The growth cycle pushes the economic and stock market upward through a combination of demographics, technology, and economic prosperity. At one point, the growth is no longer organic enough, so it has to raise more debt to keep growing. Just like a snake devours itself to grow bigger, but ends up hurt itself.

- Then the hawk represents the force that would come down to disrupt and stop the serpent from destroying the organic growth of the cycle. The forces include deflation, debt default, helicopter money, …etc. Once any of these forces come down for the serpent, the stock market would start tumble, cracking a wall of growth and stepping into the time of declination of your portfolio value.

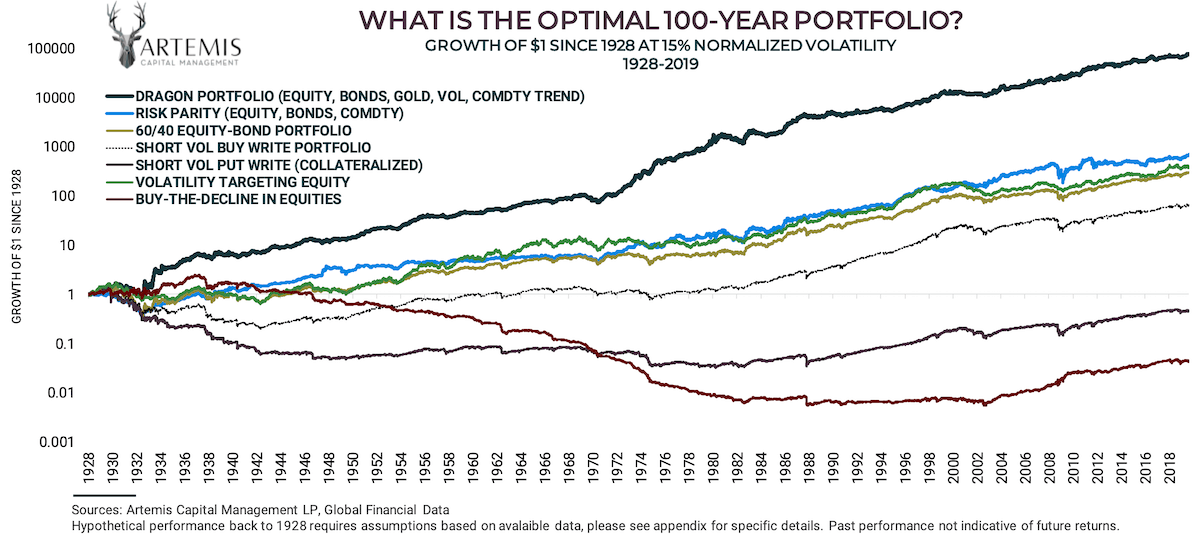

So what should people do to construct a portfolio that lasts 100 years and mitigates the impact of a hawk?

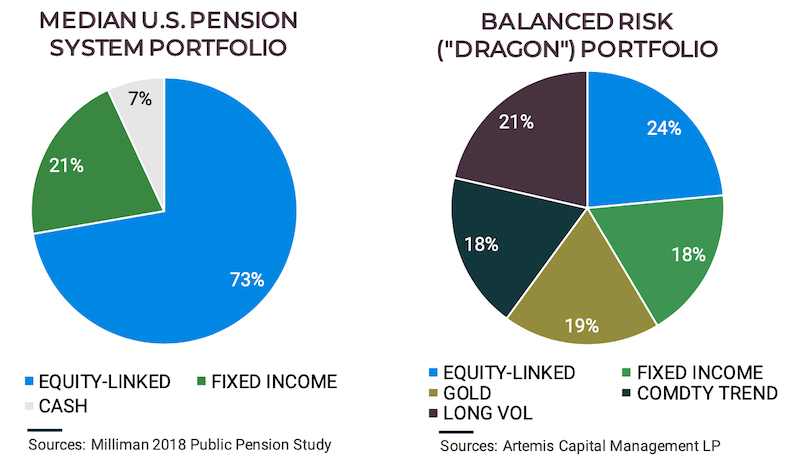

The solution - Dragon portfolio

What is dragon portfolio

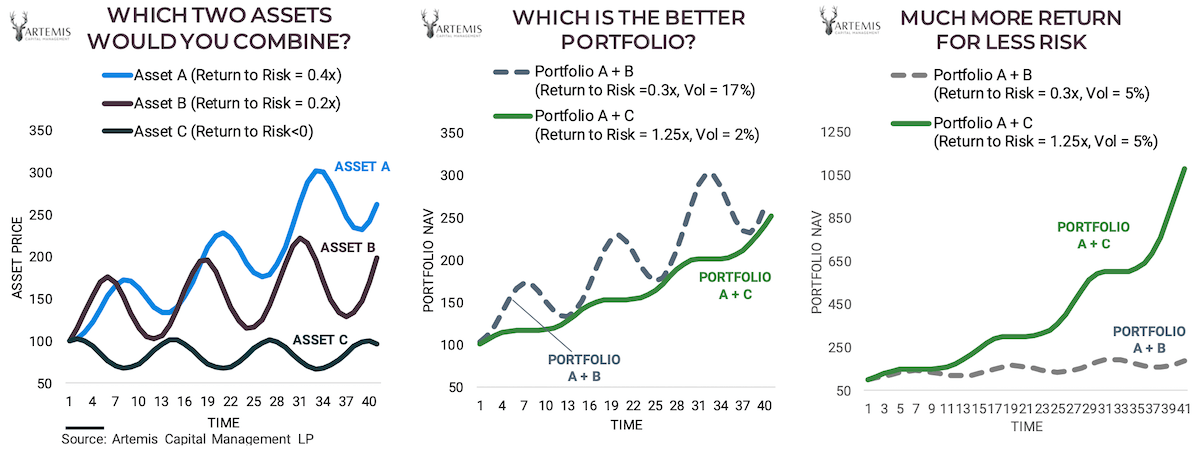

As illustrated above, asset A and asset B are quite similar in terms of the stock price movement, meaning they are correlated. Asset A and C and asset B and C are less correlated to each other. As asset A and asset C have low correlation, the portfolio A + C that has less risk (compares to portfolio A + B) will generate more profits from the portfolio built, whereas the downward price movement of asset A was offset by the slightly upward price movement. To make the outcome much easier to understand, make more money with less risk.

The law of cosmic duality proves that, counter-intuitively, a defensive asset can be precious to the total portfolio, even if it fails to make money consistently.

So how to build your investment portfolio and also your own retire financial plan? The solution suggested is fairly simple: find assets that can perform when Stocks and Bonds collapse, and boldly own them regardless of short term performance. However, what’s that different from the traditional 60/40 equity bond that helps you hedge the downside risk? The key to superior portfolio returns is to make surprisingly LARGE allocations to alternative assets that perform when Stocks and Bonds start sliding.

The centerpiece of the book: Anti-correlation is worth more than excess return

Asset classifications

In the paper, it also introduced each asset class that we can use to construct the dragon portfolio out of them. I will let you read those from the article as it’s redundant to put those words again in this article.

- Serpent assets that profit from secular growth and stability

- Equity Market

- Real Estate

- Corporate Bonds

- …

- Hawk assets that profit from secular change

- Active Long Volatility

- Commodity Trend Following Strategy

- …

- Hawk assets that profit from monetary debasement

- Gold, Gold ETF

- High-quality Bonds

Challenges to construct the portfolio that protects your assets from depreciating in the next 100 years

As mentioned in the article here, that people tend to follow the herd, which called Herd Behavior. As we’re born to be humans, we are biologically programmed to be part of a group. The normal investors are not emotionally strong or brave enough to buy stocks that others think unpromising. It is not intuitive to reallocate gains from a performing asset to something that hasn’t made money in a decade.

So the challenges would be social instead of financial. Say, when you have put over 60% of your assets into bonds and fixed income that generate 1~3% profit annually while you’re friends have made 6~10% per month with equity, the temptation of giving it a shot would be quite substantial for one person to allocate more money in the equity market.

That is where the nightmare starts….